Google & Apple Stock Price Analysis

Interactive Power BI Dashboard · Financial Insights (2005–2025)

Project at a Glance

A dynamic Power BI dashboard comparing Apple (AAPL) and Google (GOOGL) stock performance over 20 years. Explore volume trends, daily returns, cumulative gains, and risk via interactive slicers.

View on GitHubData & Scope

- Dataset: World Stock Prices (Kaggle, Yahoo Finance)

- Market: United States

- Companies: Apple (AAPL) & Google (GOOGL)

- Granularity: Daily (2005–2025)

Data Preparation

Transformed raw CSV in Power Query for precision:

- Split date/time via delimiter for hierarchies.

- Filtered to USA/Apple/Google only.

- Removed 0-volumes for log scaling.

- Added Daily Return Column:

DIVIDE([Close] - [Open], [Open])(% change). - Date filter: 2005–2025 (Google does not contain data before 2005).

Dataset Source

Tools & Skills

Key DAX Measures

Cumulative Return

Tracks overall gains/losses over time.

Cumulative Return =

VAR CurrentDate = MAX([Date])

RETURN

CALCULATE(

SUM([Daily Return]),

FILTER(

ALL([Date]),

[Date] <= CurrentDate

)

)Volatility Target

Target:

0.015Rolling Volatility

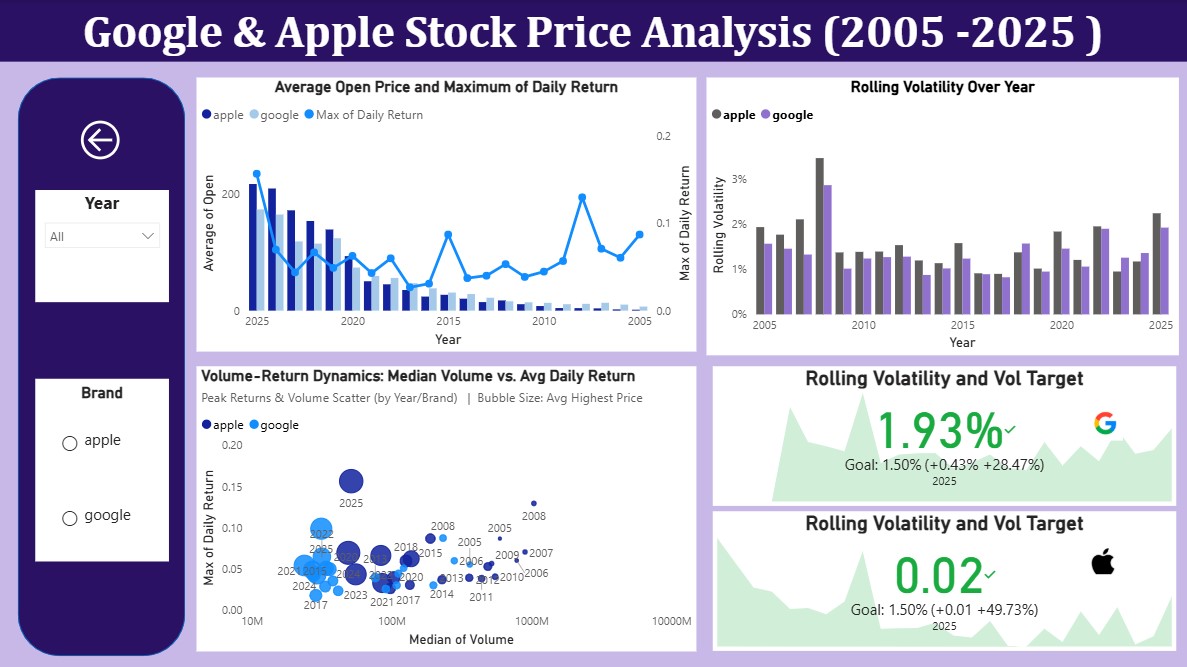

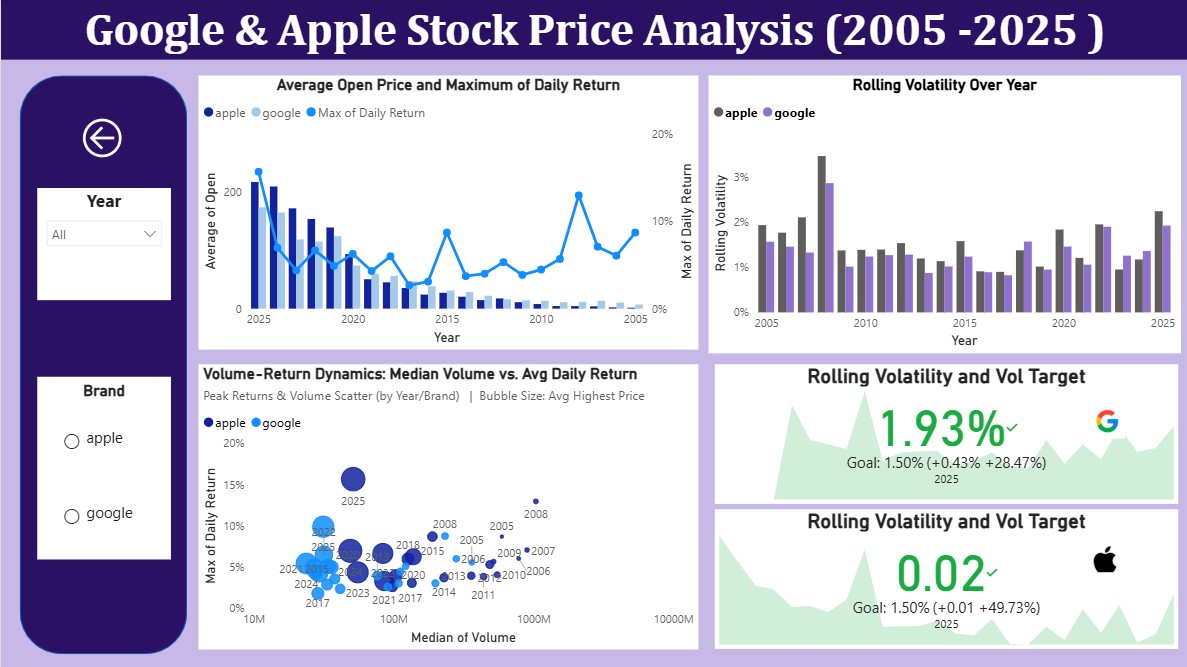

Implemented KPI cards to benchmark Apple and Google rolling volatility against a 1.5% target, enabling quick visual comparison of relative risk levels across time.

Rolling Volatility =

VAR CurrentDate = MAX('World-Stock-Prices-Dataset'[Date])

VAR LookbackDays = 252

VAR AvailablePeriod =

CALCULATE(

COUNTROWS('World-Stock-Prices-Dataset'),

ALL('World-Stock-Prices-Dataset'[Date]),

'World-Stock-Prices-Dataset'[Date] <= CurrentDate

)

VAR ActualDays = MIN(LookbackDays, AvailablePeriod)

RETURN

IF(

HASONEVALUE('World-Stock-Prices-Dataset'[Brand_Name]),

IF(

ActualDays >= 30,

CALCULATE(

STDEV.P([Daily Return]),

ALL('World-Stock-Prices-Dataset'[Date]),

DATESINPERIOD(

'World-Stock-Prices-Dataset'[Date],

CurrentDate,

-ActualDays,

DAY

)

),

BLANK()

),

BLANK()

)Std dev of daily returns over 252-day window (short-term risk). Dynamic for early years.

Key Insights

Declining Trading Volume

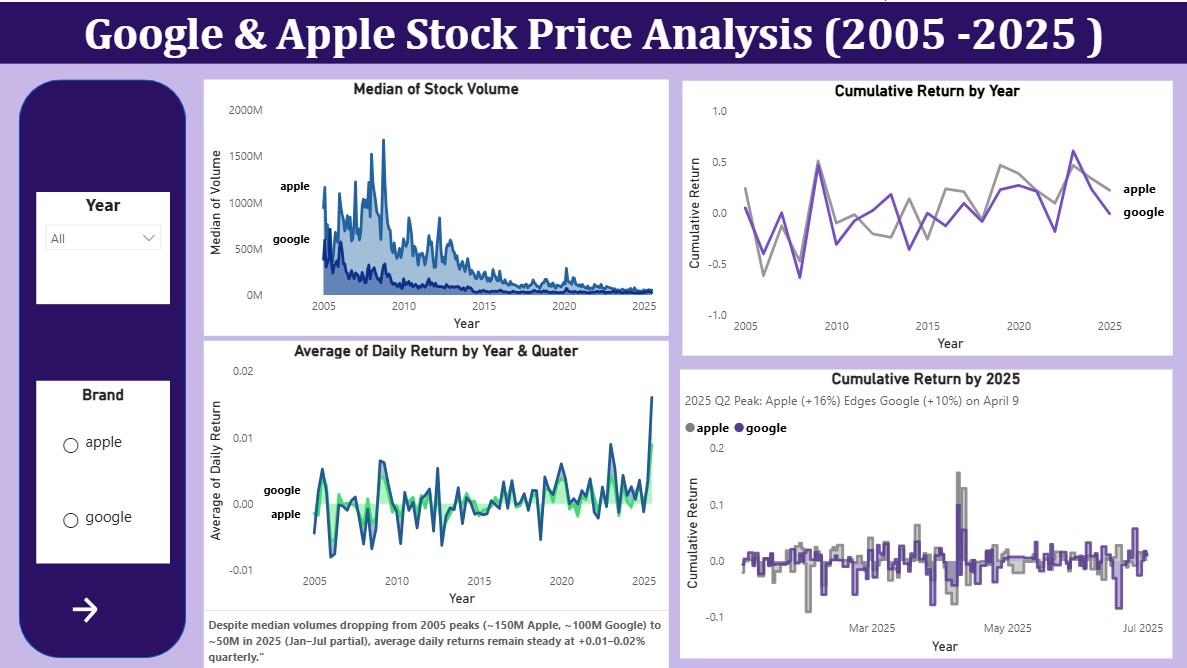

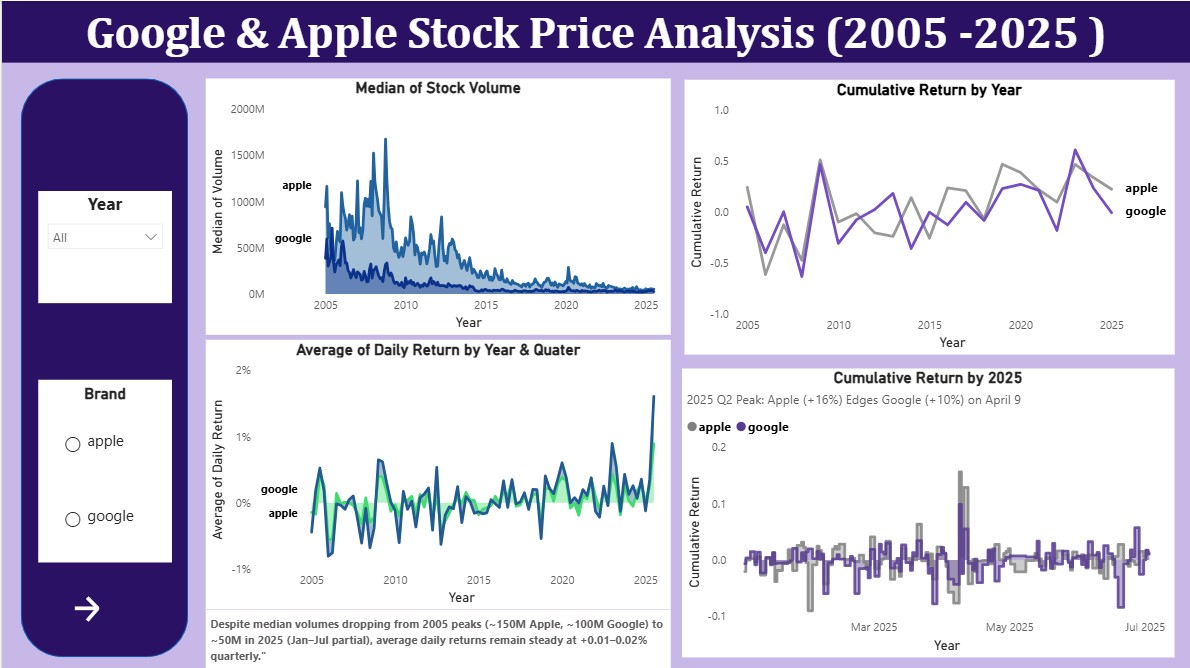

Trading volumes declined steadily from early highs (Apple ~150M, Google ~100M in 2005) to around ~50M by 2025 (partial data). This suggests market maturity and increased institutional trading rather than reduced investor interest.

Stable Daily Returns

Despite falling volumes, daily returns remained stable at approximately 0.01–0.02%. In 2025 (partial), Apple recorded a peak daily return of +0.16%, while Google peaked at +0.10%, indicating efficient price movement even with lower trading activity.

Strong Cumulative Performance

The highest cumulative returns were observed in Q2 2025, with Apple gaining approximately 16% and Google about 10%. This period highlights a strong rebound in the technology sector.

Market Risk & Volatility

Rolling volatility peaked during the 2008 financial crisis at around 3–4%. In contrast, volatility in 2025 stabilized near 2%, remaining slightly above the 1.5% target but well below crisis levels, indicating controlled market risk.

Note: 2025 data covers January–July only. Overall, Apple and Google show closely correlated price movements, with Apple demonstrating marginally higher return efficiency.